Preliminary view – PROUT analysis

Introduction

The emergence of decentralized cryptocurrencies has prompted renewed debate regarding the nature of money. Advocates describe systems such as Bitcoin as ‘trustless money’, superior to state-issued currency. Critics argue they are simply token assets (and thus property) and can also be volatile speculative instruments lacking monetary fundamentals.

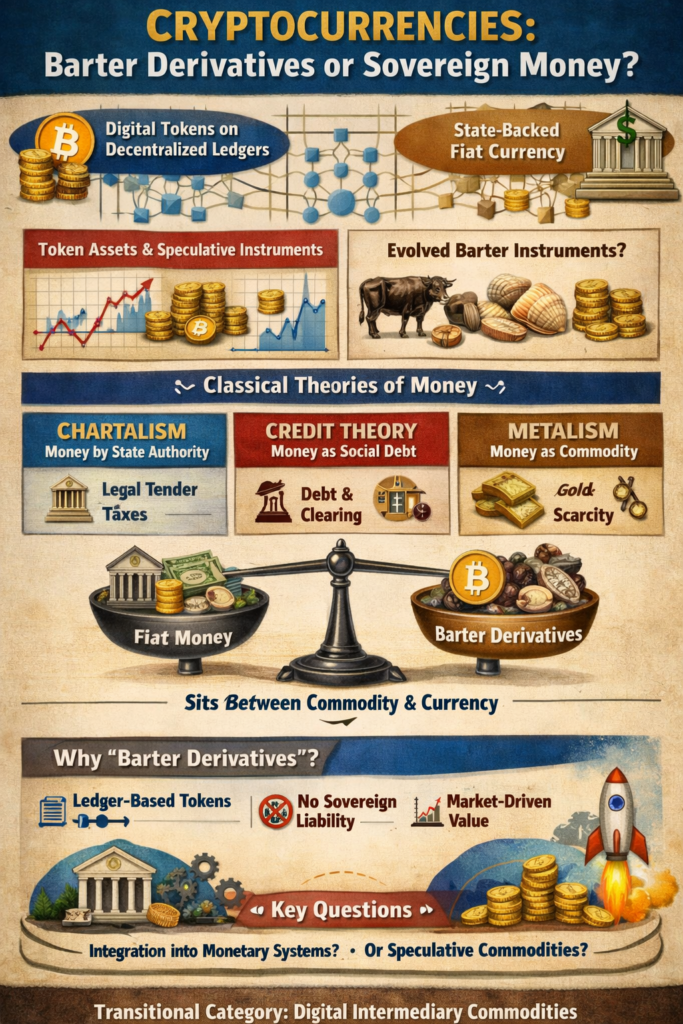

Cryptocurrencies such as Bitcoin may be understood not as fully developed money, but as barter derivatives, that is, digital intermediary commodities that resemble evolved barter instruments rather than sovereign currency. Drawing on metalist, chartalist, and credit theories of money, and informed by the ‘keep money circulating’ maxim recognised by PROUT, it can readily be argued that cryptocurrencies lack the institutional, legal and debt-clearing characteristics that define modern fiat money. In this regard, while technologically innovative, cryptocurrencies function primarily as digital commodities whose value depends on exchangeability rather than embeddedness in a social contract of productive circulation of money in the economy and taxation that goes with it.

Therefore, cryptocurrencies occupy a transitional category between commodity money and financial asset, best conceptualized as barter derivatives within contemporary monetary theory. This is a conceptual clarification. That is, cryptocurrencies function structurally as digital intermediary commodities facilitating exchange outside sovereign monetary systems, rather than as fully developed money embedded in a social contract.

This argument proceeds through an examination of:

- Classical theories of money, i.e. metalism, chartalism, credit theory.

- Institutional definitions of modern money.

- The distinction between intermediary goods and debt-based currency.

- The implications of circulation and social contract theory.

Theoretical Foundations of Money

Under the ‘keep money circulating’ framework, the characteristics of money are as follows:

- a medium of exchange,

- a store of value,

- a unit of account,

- a standard of deferred payment.

However, beyond these functional criteria, there are deeper structural characteristics. This can briefly be analysed through three theories of money. They are as follows.

1 Chartalism: Money as State Creation

Chartalist theory holds that money derives value from the following:

- state backing and monetary governance,

- legal tender status,

- tax obligations payable in the state’s currency.

Under this view, money’s demand is institutionally embedded and tax-driven. Modern Monetary Theory (MMT) extends this insight. It argues that sovereign issuers of fiat currency cannot ‘run out’ of money, as they are monopoly issuers of the unit in which taxes are imposed.

Cryptocurrencies do not meet these criteria. They do not represent sovereign monetary authority. Nor are they generally accepted for tax payments.

2 Credit Theory: Money as Debt

Alfred Mitchell-Innes’ credit theory defines money as a social debt relationship, with the following characteristics:

- it is a liability of an issuer,

- it represents a claim on society,

- it functions as a clearing instrument for obligations.

Fiat currency extinguishes debt because it is legally recognized as final settlement. When a debtor pays in fiat currency, the creditor cannot refuse it if it is designated as legal tender for that obligation. This legal status gives fiat money its central role in modern monetary systems and in the discharge of contractual obligations.

Bitcoin, by contrast, has the following characteristics:

- is not a liability of any institution,

- does not represent a debt claim,

- does not settle tax obligations (in most jurisdictions).

Thus, Bitcoin and cryptocurrencies do not function as money in the credit-theory sense. They do not extinguish debts by legal authority in the way a state-issued currency does. Instead, cryptocurrencies operate primarily as transferable digital assets whose acceptance depends on voluntary agreement rather than legal tender status.

3 Metalism: Commodity Foundations

Metalist theory historically grounded money in intrinsic value, for example, based on gold or silver, so commodity money was considered as having:

- scarcity,

- durability, and

- market value independent of state decree.

Bitcoin resembles this model superficially, as it has:

- artificial scarcity (with a 21 million cap),

- mining-based issuance (algorithmically predetermined through proof-of-work consensus), and

- a market-determined price (formed through supply and demand in open trading).

While even bullion was historically embedded within sovereign money systems and convertibility regimes, it derived its monetary function from state recognition and legal frameworks governing convertibility into coins or notes. Bitcoin lacks such institutional anchoring. Its value and acceptability depend primarily on market consensus rather than sovereign authority or legal tender status. There is no monetary authority, and it is not created through credit/lending or central bank policy.

From Barter to Intermediary Commodities

Generally, early exchange systems relied on a mix of the following:

- gift economies (with reciprocation),

- bilateral barter (which later extended to plurilateral or multilateral barter),

- intermediary commodities (shells, cattle, salt).

These intermediary commodities were not money in the modern sense. They were accepted because they could later be exchanged again. They derived value from expected future exchange, not from legal or institutional backing.

Cryptocurrencies structurally resemble these intermediary goods in the following ways:

- Their value depends on market participants’ willingness to accept them.

- They circulate based on network belief (which is not related to tax enforcement).

- They do not extinguish sovereign obligations.

Thus, cryptocurrencies have a similarity to, and are digital successors to, intermediary barter commodities. They function as exchange media accepted by some participants, but without the legal or institutional backing that characterizes sovereign money. Their circulation therefore depends on voluntary acceptance within networks rather than on a state’s authority to designate final settlement.

Why ‘Barter Derivative’?

The term barter derivative captures three structural features:

1 Derivation from Exchangeability and Ledger Balances

Bitcoin’s value depends on the expectation that:

- others will accept it in future exchange, and

- market liquidity persists.

This mirrors commodity barter intermediaries. Like earlier intermediary commodities such as salt, cattle, shells or precious metals, cryptocurrencies can circulate as widely accepted exchange goods without possessing the legal status of sovereign money. As mentioned, their acceptance depends on shared expectations among participants rather than formal state authority.

Furthermore, like early barter systems holding a cryptocurrency is derived from maintaining ledgers. Barter systems, particularly plurilateral and multilateral, also maintained ledgers through record-keeping such as tally sticks, clay tablets, or written accounts kept by merchants or community authorities, or even at temples, to track obligations and exchanges among participants. The balance of account is like a derivative, which has value and can be represented as a virtual token. However, unlike historical barter commodities and ledger-keeping, cryptocurrencies rely on distributed digital ledgers to record and verify transactions across a network, replacing physical possession with cryptographic accounting.

2 Absence of Embedded Debt-Clearing

Unlike fiat currency, the following apply to cryptocurrencies (including Bitcoin):

- they do not represent a social liability,

- they do not form part of M1 or M2 monetary aggregates,

- they do not arise through bank credit creation.

They are external to the credit system. In the credit theory of money, monetary aggregates such as M1 and M2 represent different layers of credit claims within the financial system. M1 typically includes the most liquid forms of money, being currency in circulation and demand deposits because these are immediately usable to settle debts. M2 expands this by including savings deposits and certain short-term financial instruments, which are also claims on the banking system but slightly less liquid. Within a credit-based monetary system, much of the money included in these aggregates is created through bank lending, meaning deposits represent credit relationships between banks and their customers. Thus, monetary aggregates measure the scale and liquidity of the credit structure underlying modern money.

3 Commodity-like Dynamics

Regulators frequently classify Bitcoin as a commodity, which is evident by the following:

- Bank for International Settlements, which has described cryptocurrencies as speculative crypto-assets.

- International Monetary Fund, which treats cryptocurrencies as digital assets rather than currency.

- In U.S. market regulation, where Bitcoin falls under commodity oversight.

Furthermore, commercial accounting standards treat crypto holdings as intangible assets. In accounting frameworks, they are therefore recorded similarly to other non-monetary digital property rather than as cash or cash equivalents. This reinforces the interpretation of cryptocurrencies as tradeable commodities rather than sovereign money.

Circulation and the Social Contract

The ‘keep money circulating’ framework emphasizes that the value of money increases with its mobility. When money continuously circulates through transactions, it supports economic activity, particularly production, distribution and consumption, as well as employment. Conversely, when money is hoarded or removed from circulation, it can reduce demand and slow economic exchange. Today, financial intermediaries such as banks help mitigate the problem of non-circulation by recycling deposits into loans and investments, although this mechanism does not always fully prevent money from remaining idle within the financial system.

Accordingly, modern fiat money is embedded in and subject to:

- banking intermediation,

- credit expansion,

- prudential regulation,

- monetary policy, and

- tax-driven demand.

Cryptocurrency culture, however, frequently promotes:

- hoarding (HODL = hold on for dear life),

- deflationary scarcity (fixed supply narratives such as the 21 million Bitcoin cap intended to increase long-term value), and

- price appreciation narratives (expectations that rising market demand will drive continual increases in token prices, i.e. the derivative).

This dynamic aligns more closely with commodity accumulation than with circulation-based monetary systems. In such cases, the asset or commodity is often valued primarily for its potential to appreciate rather than for its role as a medium of exchange. If money’s economic value increases with mobility, then deflationary hoarded assets may weaken productive circulation.

Other Cryptocurrency Factors

Proponents argue that Bitcoin and cryptocurrencies generally:

- Are trustless, because transactions are verified by cryptographic consensus on a decentralized blockchain (distributed ledgers) rather than by trusting a central authority or intermediary.

- Eliminate reliance on central banks, because issuance, transaction validation, and monetary supply are governed by predetermined protocol rules and distributed network consensus rather than by discretionary monetary policy or centralised institutional control.

- Enable peer-to-peer settlement, because participants can transfer value directly between digital wallets over the network without requiring banks, payment processors, or other intermediaries to clear or settle the transaction.

However, economic trust is still required in relation to cryptocurrencies. This refers to the confidence participants place in the system’s technology, code, rules and network consensus mechanisms to reliably record ownership and execute transactions without relying on a central authority. Accordingly, ‘trustless’ in technical terms does not eliminate economic trust. It merely shifts trust from institutions to:

- code,

- network consensus, and

- market belief.

Moreover, widespread price volatility undermines a cryptocurrency’s unit-of-account function. When prices fluctuate rapidly, goods and services cannot be reliably denominated in the cryptocurrency. As a result, economic actors want to and tend to price transactions in stable fiat currencies and so treat the cryptocurrency primarily as a speculative asset rather than a standard measure of value.

Even in El Salvador, where Bitcoin had legal tender status (between 2021 to 2025), usage remained limited relative to fiat circulation. Since 2001 until today, the official currency used in El Salvador is the United States dollar. Even when Bitcoin was legal tender, most businesses and consumers continued to rely primarily on the United States dollar for pricing, wages and daily transactions. Low adoption of Bitcoin, as well as price volatility and concerns from international financial institutions, such as the International Monetary Fund, led the government to amend the law so that acceptance of Bitcoin was no longer mandatory for businesses. As a result, while Bitcoin technically remained usable, its legal tender status was effectively reduced and its role in everyday payments declined significantly.

A Transitional Category

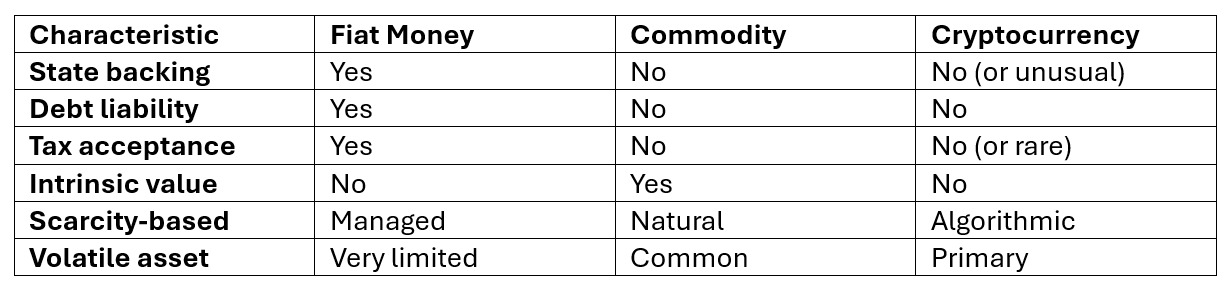

Considering the above, cryptocurrencies in relation to fiat money and commodities occupy a space for transactional purposes as follows:

| Characteristic | Fiat Money | Commodity | Cryptocurrency |

| State backing | Yes | No | No (or unusual) |

| Debt liability | Yes | No | No |

| Tax acceptance | Yes | No | No (or rare) |

| Intrinsic value | No | Yes | No |

| Scarcity-based | Managed | Natural | Algorithmic |

| Volatile asset | Very limited | Common | Primary |

Cryptocurrencies are not pure commodities, nor fully institutional money. They are digital intermediary exchange tokens for which maintaining ledgers is crucial. As they are intended also for transactions purposes, they can be considered as barter derivatives. Their economic role sits between speculative asset and experimental payment mechanism, lacking the institutional foundations that historically transform exchange media into sovereign money.

Conclusion

Modern money is best understood as an institutionalized system of credit and settlement anchored in state authority, banking networks, and legally enforceable obligations. This is crucial because it explains why modern currencies function as universally accepted means of payment capable of reliably extinguishing debts within a legal and economic framework. Cryptocurrencies such as Bitcoin do not satisfy the structural criteria of modern money under either metalist, chartalist or credit theories. They do not:

- represent sovereign liability, as they are not issued or guaranteed by the state or backed by its legal authority,

- function as socially and economically embedded debt-clearing instruments, or

- extinguish tax obligations, such as payment of taxes, fees and other impositions that amount to liabilities of a person.

Instead, they operate as:

- scarce digital commodities, though the extent of this varies depending on protocol design and issuance rules,

- market-priced assets, with values determined by supply and demand in trading markets, and

- intermediary exchange objects, used by participants as transferable media of exchange within voluntary networks.

Given that cryptocurrencies:

- are tradable digital tokens representing balances recorded on decentralized ledgers,

- function as intermediary exchange objects to enable indirect exchange of goods and services through transferable ledger entries,

- are not credit instruments, and

- could be used as a security,

they can be understood as distributed-ledger barter derivatives. In this sense, cryptocurrencies reproduce the economic role of historical barter intermediaries, but in a digitized, tokenized and cryptographically verified ledger environment rather than through physical commodities. They resemble digitally evolved intermediary commodities more than sovereign money embedded in social contract and credit structures. Thus, the proposition that cryptocurrencies are barter derivatives is theoretically defensible.

Whether they evolve further toward institutional integration (socially and economically), or remain near to speculative digital commodities, remains an open question. Much will depend on regulatory frameworks, technological developments, and the willingness of financial institutions and states to incorporate them into existing monetary infrastructures. Their long-term role will also hinge on whether they can achieve stable economic functions beyond speculative trading and niche payment uses.

https://open.substack.com/pub/macropsychic/p/cryptocurrencies-as-barter-derivatives